1. Taxpayers can now file returns for AY 2023-24 through Income Tax Return (ITR) forms ITR-1 and ITR-4 on the e-filing portal in online mode with pre-filled data.

2. Responding to concerns of taxpayers over the imposition of 20% TCS on International Credit Card and Debit Card transactions under the Liberalised Remittance Scheme (LRS) from July 1, the Central Government said no TCS will be collected on small transactions up to Rs 7 lakh.

3. The Directorate of Income Tax (Systems) has issued a User Guide for Submitting Response to Notices and Letters Received under the e-Verification Scheme, 2021 Version 1.0.

4. The Directorate of Income Tax (Systems) has issued FAQs for Submitting Response to Notices and Letters Received under the e-Verification Scheme, 2021.

5. GSTN Enables Functionality to Find Invoice Reference Number (IRN) through Document Number dated May 18, 2023. It is to inform you that the Goods and Services Tax Network has introduced a new function that allows users to find the Invoice Reference Number (IRN) by using the Document Number.

6. No Service Tax on User Development Fees Collected by International Airport being a ‘statutory-levy’: Supreme Court of India.

7. MCA has set up a Right to Repair portal that allows citizens to get their gadgets and vehicles repaired without losing their warranty.

The portal is now live and currently covers four sectors – consumer durables, electronic devices, automobiles, and farm equipment.

8. Sebi proposed in a consultation paper that if a share in the futures and options segment falls or rises by 10% a day, trading would be suspended for an hour, up from the current 15 minutes, and then allowed to move only a further 2%, down from the current 5%.

By CA Raj Chawla

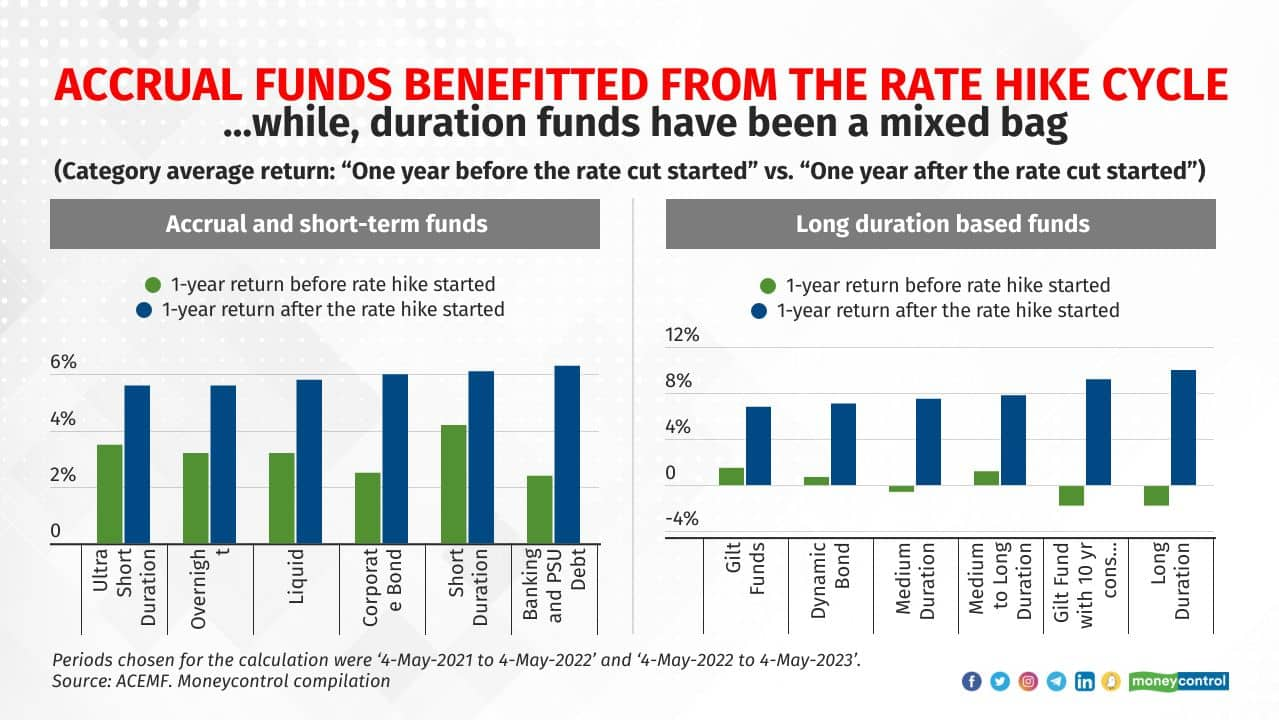

to 1.9 years and 1.5 years respectively in May 2022, down from 2.5 years and 1.9 years respectively a year ago. Similarly, gilt funds cut the portfolio duration to 2.3 years in May 2022 compared to 4.7 years in May 2022. However, as per the latest data as of April 2023, these schemes have raised the portfolio duration to 2.6 years, 2.1 years and 4.5 years respectively.")