Mr..Randeep Singh Jauhar-Mr.Bhupinder Singh Jauhar and Mr.Pradeep Singh Jauhar

Jamna Auto Industries (JAI), a leading spring manufacturer and supplier to commercial vehicles (CV) majors, has posted a strong growth in net sales and profit-after-tax (PAT) in Q1 FY19. Despite the significant rise in raw material (RM) prices, it posted operating margin expansion on year-on-year (YoY) basis.

With marquee clientele in its kitty and strong financials, the company is well placed and deserves investor attention. Recent correction in the stock has made valuations attractive for the long term.

Quarterly snapshot

In Q1 FY19, the company posted a 107.1 percent YoY growth in net revenue. It was supported by strong growth emanating from medium and heavy commercial vehicle (M&HCV) segment and low base of last year ahead of implementation of the Goods and Services Tax (GST).

Despite the significant rise in raw material prices, the company posted an earnings before interest, tax, depreciation and amortisation (EBITDA) margin expansion of 216 basis points and 146.9 percent growth in EBITDA. Margin expansion was led by operating leverage and lower operating and employee costs. Profit-after-tax (PAT) witnessed a significant YoY growth of 129.9 percent.

Key growth drivers

Dominant position

JAI has a dominant position in CV springs and commands around 69 percent market share as of Q1 FY19-end. The company supplies to who’s who of the industry.

Strong focus on R&D

The management continues to focus on R&D to continue to be ahead of the curve. In fact, it is the only company with a spring R&D centre in India. The company is investing to upgrade its information technology infrastructure, which is to be implemented across the company.

JAI gets its technical competence from its technical association with US-based Ridwell Corporation, a global leader in design and manufacturing of air suspensions and lift axles. It has also signed a technology transfer pact with Tinsley Bridge, UK.

Strong CV demand

After regulatory challenges, starting with demonetisation, followed by Bharat Stage IV implementation and GST-led disruption, CV demand has increased sharply. In FY18, it witnessed domestic volume growth of 19.9 percent versus 14.2 percent growth for the overall industry.

Despite the new axle load norms, momentum in CV demand continues. JAI, being the largest player in supplying suspension springs to CV, would continue to gain from the upcycle in this segment.

Unaffected by electric vehicle disruption

The company is likely to remain unaffected by the electric vehicle disruption going forward as the products it manufactures are immune to the adoption of EVs.

Strong aftermarket

JAL also has strong presence in aftermarket (15-18 percent market share) in India. Post-GST, the company has been witnessing strong demand in aftermarket led by a shift from unorganised to organised player due to lower price differential. It is now aggressively expanding its distribution network to touch its 30-35 percent market share target in the next couple of years.

Robust product pipeline

In an efforts to de-risk its dependence on a single product, the management continues to add new products to its kitty. Currently, it has four new products - stabiliser bar, u bolt, z spring, and trailer suspension -under development.

Adoption of parabolic leaf springs

There is an increasing adoption of parabolic leaf springs by major original equipment manufacturers (OEMs) given the need for lighter products ahead of BS VI adoption. This augurs well for JAI as it has greater dominance in that space, with over 90 percent market share.

Capacity in place

In terms of capacity, JAI is the second-largest manufacturer across the globe with an installed capacity of 240,000 units across 9 manufacturing units. The management plans to open 2 more plants to service additional demand. The company has 2 upcoming plants, 1 each in Indore and Adityapur.

Valuation at reasonable levels

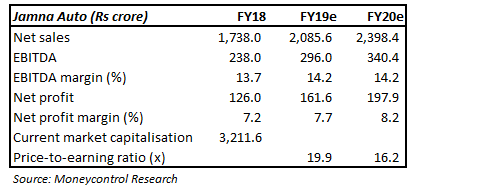

The recent correction in the stock has made valuations attractive. The stock is currently trading at 19.9 and 16.2 times FY19 and FY20 projected earnings, respectively. We advise investors to buy the stock with an eye on the long term.

No comments:

Post a Comment